IMF / GLOBAL FINANCIAL STABILITY REPORT

STORY: IMF / GLOBAL FINANCIAL STABILITY REPORT

TRT: 03:53

SOURCE: IMF

RESTRICTIONS: NONE

LANGUAGE: ENGLISH / NATS

DATELINE: APRIL 16 2024, WASHINGTON DC

RECENT - WASHINGTON DC

1. Various shots, IMF building exterior

APRIL 16 2024, WASHINGTON DC

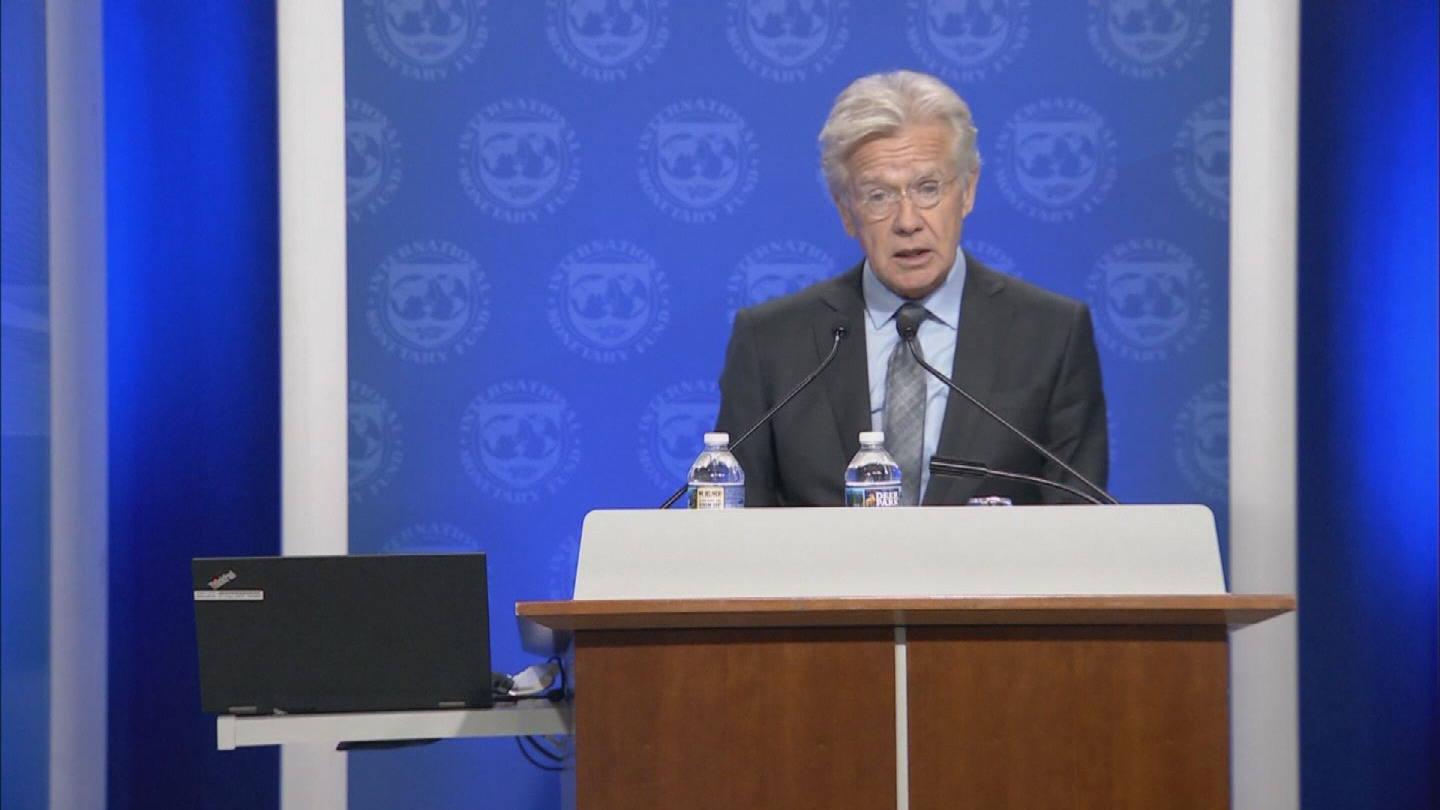

2. SOUNDBITE (English) Tobias Adrian, Director of the Monetary and Capital Markets Department, IMF:

“Global financial stability has improved since we last met in October. The backdrop is a global baseline of a soft landing with inflation gradually returning to target. Markets have been optimistic, with risky asset rallying and credit spreads compressing. Riskier borrowers have been able to issue debt and access other forms of capital market financing.”

3. Wide shot, Tobias Adrian speaking

4. SOUNDBITE (English) Tobias Adrian, Director of the Monetary and Capital Markets Department, IMF:

“Even though global financial stability has improved, we still worry about the number of short-term risks. First of all, inflation could be more persistent and hence interest rates could shoot up. Secondly, commercial real estate has been hit and the number of financial institutions exposed to declining values in commercial real estate. Thirdly, volatility in asset markets is very compressed, correlations are very high while underlying economic and policy uncertainty is still elevated. So this mismatch between asset market correlation and economic uncertainty is a worry and that could lead to repricing if negative shocks were to hit. Finally, while credit spreads have tightened. Credit defaults have actually been increasing. So there's a tension between the pricing of credit and the underlying realization of credit performance. In the medium term, we worry about the buildup of debt. Since the pandemic, debt to GDP has been increasing around the world. That includes sovereigns as well as the financial sector and non-financial borrowers such as households and corporations. Fast growing private credit is not a source of concern. While we don't see immediate red flags, we do worry that this asset class could, become, riskier as it expands in size. Finally, cyber security risks are an acute concern of financial institutions. We have not seen macro critical realizations of cyber incidents, but that could certainly be a risk going forward.”

5. Wide shot, Tobias Adrian speaking

6. SOUNDBITE (English) Tobias Adrian, Director of the Monetary and Capital Markets Department, IMF:

“Let me turn to our policy recommendations. First of all, central banks should ensure that inflation comes down, neither easing policies prematurely nor delaying them too long. Secondly, emerging and frontier economies should strengthen efforts to contain debt vulnerabilities. Third, supervisors and regulators must monitor and manage credit risk, particularly in the real estate market, in order to mitigate the impact on banks and other financial institutions. Finally, cyber threats could potentially have an impact on the broader economy. Supervisors, regulators and financial firms must strengthen cyber resilience of the financial sector.”

RECENT – Washington, DC

7. Various shots, IMF building exterior

In a press briefing in Washington, DC, the Director of the IMF’s Monetary and Capital Markets Department Tobias Adrian said that a sense of optimism has pervaded financial markets in recent months, amid investor confidence that the fight against inflation is entering its “last mile” and that central banks will ease monetary policy in the coming months.

“Global financial stability has improved since we last met in October. The backdrop is a global baseline of a soft landing with inflation gradually returning to target. Markets have been optimistic, with risky asset rallying and credit spreads compressing. Riskier borrowers have been able to issue debt and access other forms of capital market financing,” said Adrian.

There are likely to be bumps along this last mile, as the IMF shows in the latest Global Financial Stability Report. Geopolitical tensions could intensify and weigh on investor sentiments. Strains in commercial real estate have become more acute, which could increase pressure on some lenders. China’s financial markets continued to be weighed down by ongoing problems in the property sector.

“ Even though global financial stability has improved, we still worry about the number of short-term risks. First of all, inflation could be more persistent and hence interest rates could shoot up. Secondly, commercial real estate has been hit and the number of financial institutions exposed to declining values in commercial real estate. Thirdly, volatility in asset markets is very compressed, correlations are very high while underlying economic and policy uncertainty is still elevated. So this mismatch between asset market correlation and economic uncertainty is a worry and that could lead to repricing if negative shocks were to hit. Finally, while credit spreads have tightened. Credit defaults have actually been increasing. So there's a tension between the pricing of credit and the underlying realization of credit performance. In the medium term, we worry about the buildup of debt. Since the pandemic, debt to GDP has been increasing around the world. That includes sovereigns as well as the financial sector and non-financial borrowers such as households and corporations. Fast growing private credit is not a source of concern. While we don't see immediate red flags, we do worry that this asset class could, become, riskier as it expands in size. Finally, cyber security risks are an acute concern of financial institutions. We have not seen macro critical realizations of cyber incidents, but that could certainly be a risk going forward,” added Adrian.

Financial regulatory authorities should take steps to ensure banks and other institutions can withstand defaults and other risks, using stress tests, early corrective actions, and other supervisory tools.

“Let me turn to our policy recommendations. First of all, central banks should ensure that inflation comes down, neither easing policies prematurely nor delaying them too long. Secondly, emerging and frontier economies should strengthen efforts to contain debt vulnerabilities. Third, supervisors and regulators must monitor and manage credit risk, particularly in the real estate market, in order to mitigate the impact on banks and other financial institutions. Finally, cyber threats could potentially have an impact on the broader economy. Supervisors, regulators and financial firms must strengthen cyber resilience of the financial sector,” explained Adrian.